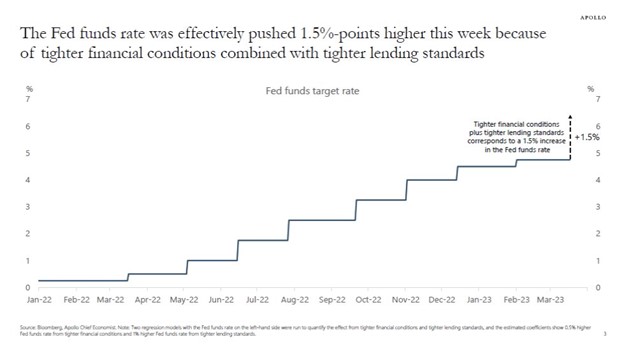

Last week, Apollo Global Management’s Torsten Slok mentioned that the events of the last two weeks will lead to tighter financial and lending conditions equivalent to a 1.5% Fed Funds rate hike. This, of course, on top of the fastest move in rate hikes—ever—with more likely to come in an attempt to curb inflation.

Actions certainly have their reactions. It turns out that nearly two decades of low-rate, free money, unprecedented and previously unimaginable money printing combined with generationally high inflation and the fastest velocity of rate hikes ever by the same people who said inflation was transitory has generated a reaction.

I mean, who would’ve thought?

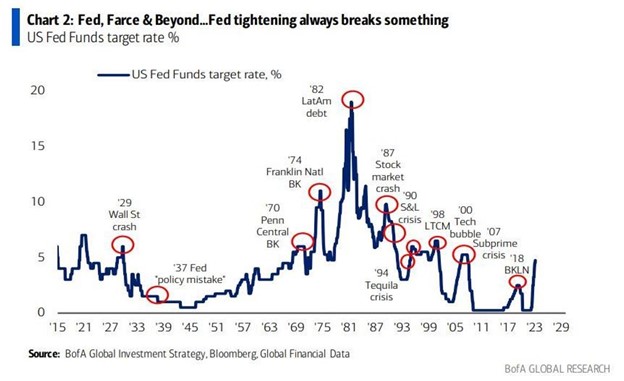

Michael Harnett from BofA points out that the Fed famously and reliably has a tendency to break things when they raise target rates quickly.

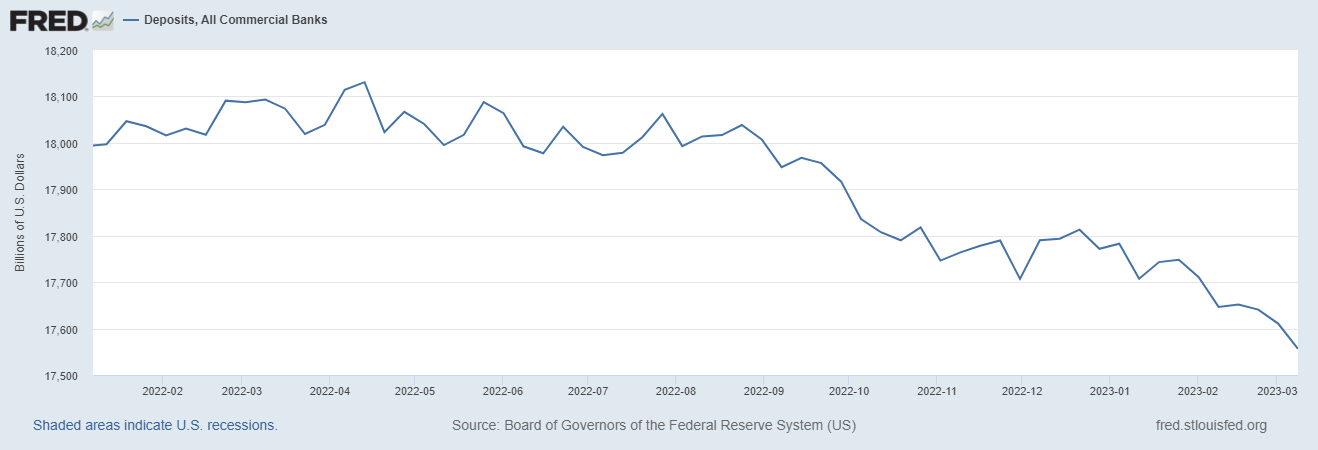

Prior to the SVB failure, bank deposits were shrinking—even at the biggest banks. Why would you keep money in a bank paying close to nothing when you can buy short-term U.S. backed treasury bonds for 4%? You wouldn’t, so bank deposits take flight. Then, as the Fed raises interest rates to combat inflation, a slower economy and more expensive money leads to consumers and business having less money to keep in a bank. So, deposits take flight across the whole system all at the same time.

As a result, the bank system’s once fortress-like liquidity and balance sheet position gets less secure very quickly. While this is not 2008 and most banks are strong enough to take this punch, the management team of banks are forced to navigate an environment where their liquidity (cash available to service their obligations) is falling and asset values (the value of loans and investments affected by rapid rate increases) are declining.

Adding insult to injury, in 2021, all the government types were telling banks (and everyone else for that matter) not to worry about transitory inflation and to go ahead and use all those surplus deposits to buy ‘safe’ treasuries, essentially financing the government money printing for them only to discover later, inflation wasn’t transitory at all. In fact, those same government types would change their tune and raise rates faster than ever before to combat a problem they said wasn’t a problem.

And that creates–a problem–because all those treasuries banks bought in 2021 are now underwater and the only way they get whole is to hold to maturity. As long as no deposits run off, they won’t have to sell those bonds at a loss to generate liquidity. As long as markets don’t become panicked on the mark-to-market implications of asset values across the entire sector, it’ll be ok. But of course, that’s exactly what’s happening and SVB (while the worst actor) wasn’t the only one.

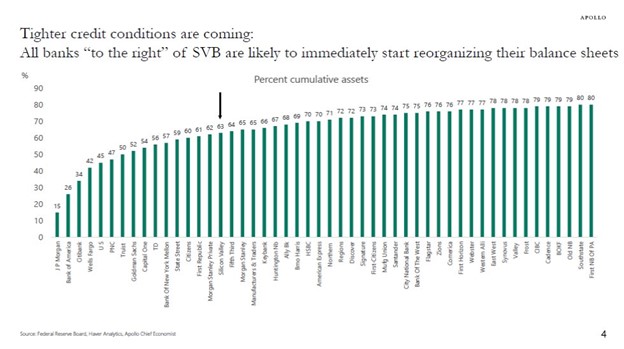

In the chart below, Apollo points to the number of large and well-regarded banks facing a strong concentration of uninsured deposits. As you can see, the issue hangs over most of the industry.

So, now what?

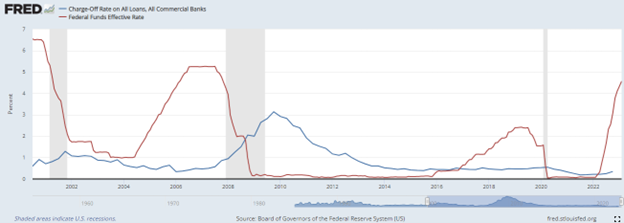

Banks need to drive new liquidity fast in the environment where all deposits are shrinking or they have to get hyper conservative, really quickly, on what investments or loans they make. Keep in mind low interest rates have pushed banks to find yield in a low rate environment, and most regional banks generate yield through their loan portfolio. Higher yield generally equates to higher risk when it comes to lending. The next “shoe to drop” is the increase in default rates and charge offs in bank loan portfolios amid a slowdown in the economy, causing borrowers to have less liquidity and cash available to service debt obligations, and the free-flowing economy with an appetite for risk and growth prospects comes to a screeching halt.

And that, my friends, is where we are.

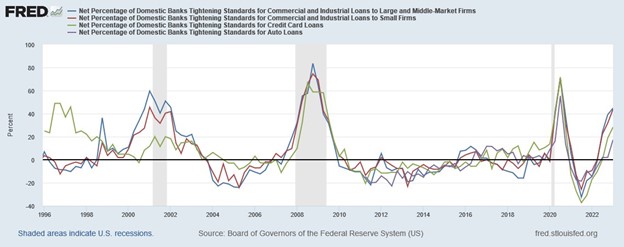

Here are more charts that demonstrate we are clearly in for credit tightening:

FED: Net Percentage of Banks Tightening Credit Standards for Commercial and Industrial Loans to large and mid-sized businesses.

Correlation of Banks Tightening to Loan Growth

FED: Rising Default Rates on C&I Loans

FED: It’s not just in middle-market and large corporate C&I. It’s a systemic tightening of credit.

*NOTE: The Feds policies have fabricated a lending and investment market that have protected lenders and investors from material losses. Positive economic trends mask poor underwriting because abundant capital seeking returns finds the risk. As the market tightens, and capital is constricted, sub-par underwriting practices become quickly exposed without options to offload those investments to other traditional capital resources willing to take the risk. When this happens and charge-offs loom, banks tighten and non-bank lenders emerge to fill the gap. The tighter and steeper the economic decline, the greater “access to capital gap” companies face.

The banks with the most ability to extend capital will be the systemically important banks (“Too Big To Fail”) that are gaining tons of deposits right now, but that doesn’t mean they will extend capital. As noted in a recent article published by Goldman Sachs, “Banks with less than $250 billion in assets comprise about 50% of U.S. commercial and industrial lending”. When you combine all of the aforementioned issues with the fact their balance sheets and loan portfolios will now be under the magnifying glass, competition for earning your business from banks wanes.

So, be careful about where you place your eggs.

Less competition for your business is not good for you and ‘keeping all your eggs in one basket’ may no longer be viable or smart. We believe credit tightening is not coming. It’s here. It just might take time to feel it and when you do it may be too late.

More than ever before, diversifying sources of capital or exploring those possibilities may be in order. In the coming days we’ll write more of the best practices of doing this, but for now, know that First National Capital has been playing the role of a diversification resource with capabilities that extend beyond traditional financing for nearly twenty years and through the barrage of these macroeconomic peaks and valleys in recent years. We’re here to help.

Folks, these events are disturbing, for sure, and while not a harbinger of impending market collapse or doom, a not-so-enjoyable change is on the horizon. Don’t take our word for it. Read the charts.

The only bad option for what’s next is not to understand your options.

Ben Frank

Chief Revenue Officer

First National Capital Corporation

Links to Data Sources

- https://www.reuters.com/markets/us/financial-or-price-stability-fed-faces-calls-pause-2023-03-18/

- https://www.marketwatch.com/story/based-on-history-the-next-bull-market-is-just-months-away-and-could-take-the-s-p-500-to-6000-says-bofa-11655475414

- https://fred.stlouisfed.org/series/DPSACBW027SBOG#

- https://twitter.com/carlquintanilla/status/1635963831192100864

- https://fred.stlouisfed.org/series/DRTSCILM

- https://fred.stlouisfed.org/series/H8B1023NCBCMG#0

- https://fred.stlouisfed.org/series/CORALACBN

- https://fred.stlouisfed.org/series/BAMLH0A0HYM2

- https://fred.stlouisfed.org/series/DRTSCILM#0

- https://www.cnbc.com/2023/03/15/goldman-sachs-cuts-gdp-forecast-because-of-stress-on-small-banks.html